|

|

Are you maximizing all the tax benefits available to you as a homeowner?

Staying up-to-date on the latest tax rules is a smart move if you’re interested in keeping more money in your pocket, but with the recent changes from the Tax Cuts and Jobs Act, you might be a little fuzzy on exactly which credits and deductions you can take advantage of. Whether you’re a long-time homeowner or just bought your very first home, it helps to have a refresher. Let’s brush up on some of the key tax perks of homeownership, so you can make the most of your benefits this tax season.* |

|

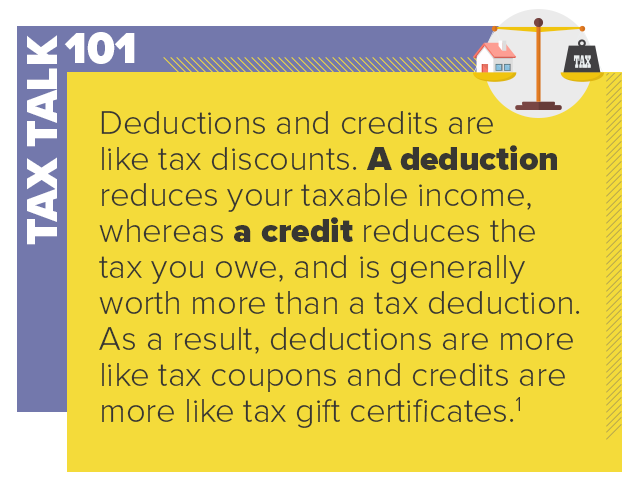

If you took out your mortgage after Dec. 15, 2017, the interest you pay on your first or second mortgage is generally tax deductible on home loans up to $750,000 (or $375,000 if married filing separately). For mortgages taken out on or before Dec. 15, 2017, the deduction applies to home loans up to $1 million (or $500,000 if married filing separately). If you took out a home equity loan or line of credit, the interest is only tax deductible if the loan was used to buy, build, or substantially improve the home that secures the loan. Exceptions, limitations, and restrictions apply, so talk to your tax advisor to see if you’re eligible for the mortgage interest deduction.2

|

|

|

Being a homeowner comes with some pretty fantastic advantages, and tax breaks are one of the benefits you don’t want to miss out on. Talk to your tax advisor to learn more about how you can max out your tax savings and get the most from your real estate investment.

|

Published on 2019-03-06 05:46:47